Submit Change to NFIP Policy: Difference between revisions

No edit summary |

No edit summary |

||

| Line 158: | Line 158: | ||

'''Example:''' A policyholder moves to a new residence and provides their updated mailing address. The agent edits the contact details in the system to reflect this change. | '''Example:''' A policyholder moves to a new residence and provides their updated mailing address. The agent edits the contact details in the system to reflect this change. | ||

{{Attention|The primary insured mailing address cannot be changed if it has been used to verify Primary Residence.}} | |||

== Renewal Billing Instructions == | == Renewal Billing Instructions == | ||

Revision as of 15:21, 7 March 2025

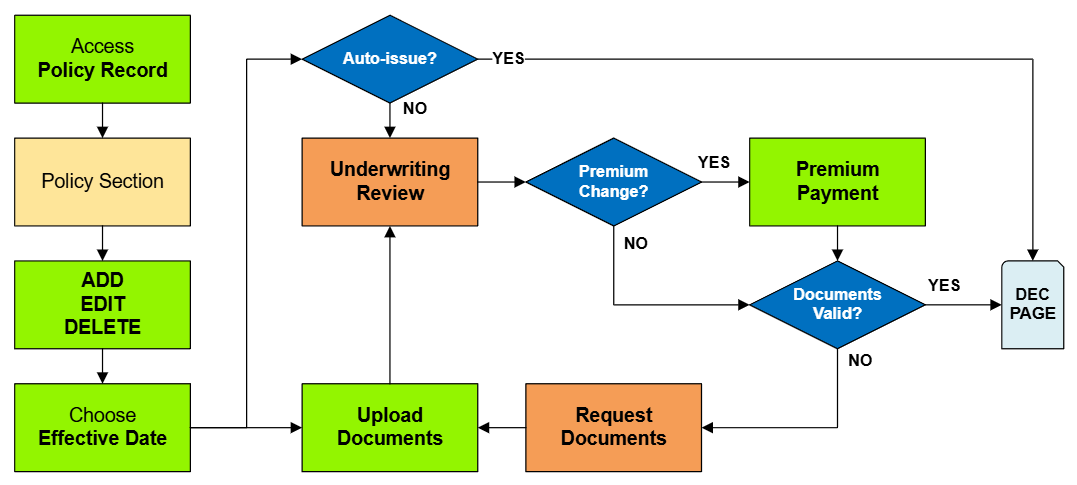

This page serves as a directory for various NFIP Policy Changes agents can request through Equinox. Each change type includes details about the process, effective dates, and required documentation. Agents can reference individual procedures for more specific instructions.

|

Policy Changes List

The table below lists the most common NFIP Policy Changes submitted by agents.

- The links in the Policy Section column will show more details about each Policy Change lower on the page.

- The links in the Functions column will go to specific procedural instruction pages.

| Policy Section | Functions | Auto-issue | Documents | Effective Date | NFIP Category |

|---|---|---|---|---|---|

| Primary Insured Contact Details | Edit | Yes | No | Request | Administrative |

| Renewal Billing Instructions | Edit | Yes | No | Request | Administrative |

| Mortgagee Clause | Add, Edit, Delete | Yes | No | Request | Policy Interests |

| Insured Name Correction | Edit | Yes | No | Inception | Administrative |

| Insured Name Update | Edit | No | Yes | Event | Policy Change |

| Additional Insured | Add, Edit, Delete | Yes | Yes | Event or Request | Policy Interests |

| Co-insured | Add, Edit, Delete | Yes | Yes | Event or Request | Policy Interests |

| Policy Assignment | Edit | No | Yes | Event | Policy Interests |

| Coverage Increase | Add, Edit | No | No | Calculated | Coverage Increases |

| Deductible Decrease | Edit, Delete | No | Yes | Calculated | Coverage Increases |

| Coverage Decrease | Edit, Delete | No | Yes | Event or Inception** | Coverage Decreases |

| Deductible Increases | Add, Edit | No | No | Event or Request | Coverage Decreases |

| Elevation Certificate | Add, Edit, Delete | No | Yes | Event or Inception | Rating Adjustment |

| Structural Variables | Edit | No | Yes | Event or Inception | Policy Change |

| Property Address | Edit | No | Yes | Event or Inception | Property Address |

| Effective Date | Edit | No | Yes | Inception | Cancel Rewrite |

| Provisional Rates | Edit | No | No | Inception | Rate Category Change |

Primary Insured Contact Details

| Functions | Auto-issue | Documents | Effective Date | NFIP Category |

|---|---|---|---|---|

| Edit | Yes | No | Request | Administrative |

Accurate contact information ensures that policyholders receive timely communications regarding their coverage, billing, and claims. Agents can update details such as mailing addresses, phone numbers, and email addresses directly in the system without additional documentation. These changes typically take effect upon request and are processed automatically.

Example: A policyholder moves to a new residence and provides their updated mailing address. The agent edits the contact details in the system to reflect this change.

Renewal Billing Instructions

This section explains how to modify billing instructions for policy renewals, including changes to payment methods or billing addresses. Proper billing information is crucial for uninterrupted coverage.

Mortgagee Clause

This section details the process for adding, editing, or removing a mortgagee clause, which specifies the rights of a lender in the event of a loss. Ensuring the correct mortgagee information is vital for compliance with loan requirements.

Insured Name Correction

This section provides guidance on correcting minor errors in the insured's name, such as misspellings. Accurate naming is essential for the validity of the policy.

Insured Name Update

This section covers procedures for updating the insured's name due to significant changes like marriage or legal name changes. Proper documentation is required to reflect these updates accurately.

Additional Insured

This section describes how to add, edit, or remove an additional insured party who has a financial interest in the property. Including all relevant parties ensures comprehensive coverage.

Co-insured

This section explains the process for managing co-insured individuals on a policy, detailing how to add, edit, or delete co-insured parties. Accurately listing co-insured parties ensures that all stakeholders are appropriately covered under the policy.

Policy Assignment

This section outlines the procedure for transferring policy ownership from one party to another, commonly occurring during property sales. Proper assignment ensures continuous coverage for the new owner.

Coverage Increase

This section provides guidance on increasing coverage limits to better protect against potential losses. Requests for coverage increases may require additional underwriting and premium adjustments.

Deductible Decrease

This section explains how to decrease the policy's deductible, which can reduce out-of-pocket expenses in the event of a claim. Lowering the deductible typically results in higher premium costs.

Coverage Decrease

This section covers the process for reducing coverage limits, which may lower premium costs but also decreases the protection level. Careful consideration is advised to ensure adequate coverage remains.

Deductible Increase

This section outlines how to increase the policy's deductible, potentially lowering premium costs. However, higher deductibles mean greater out-of-pocket expenses when filing a claim.

Elevation Certificate

This section discusses the importance of an elevation certificate in determining a property's flood risk and insurance rates. Submitting an accurate elevation certificate can lead to more favorable premiums.

Structural Variables

The building's Structural Variables are found in the Risk Characteristics section of the Policy Record.

Structural Variables can only be Edited, not Added or Deleted.

When a structural variable changes, documentation that proves the change is required.

- The Effective Date for a change is always the date the change occurred (the event date).

When a structural variable needs to be corrected, an agent statement that it was incorrect on the original application is required.

- The Effective Date for a correction is always the policy inception date.

The collapsed table below gives more details about each Structural Variable.

| Structural Variable | FIM | Details |

|---|---|---|

| Primary Residence | ||

| Occupancy* | ||

| Building Description | ||

| Detached Structures | ||

| Building Over Water | ||

| Foundation Type | ||

| Number of Floors | ||

| Number of Units | ||

| Floor of Unit | ||

| Foundation Description | ||

| Number of Elevators |

Property Address

This section provides instructions for updating the property's address information, ensuring that the insured location is correctly identified. Accurate address details are crucial for policy accuracy and claims processing.

Effective Date

This section explains how to adjust the policy's effective date, which determines when coverage begins or changes take effect. Timely updates to the effective date are essential to maintain continuous coverage.

Provisional Rates

NFIP policies issued with Provisional Rates [1] cannot be renewed. So provisionally-rated policies must be endorsed prior to the policy expiration date. Claims will also not be paid on policies with provisional rates; therefore, these policies must be endorsed before a claim payment is issued.

An agent can issue New Business or a Renewal term with Provisional rates; however, the NFIP strongly suggests that the insurer endorse the policy within 60 days of issuance. Additional premium may be required as part of this Rating Category Change.